Rental Income Tax

Rental income tax in Kenya can be a complex and confusing topic for property owners. It is important to understand the tax laws and regulations to avoid any penalties or legal issues. In this comprehensive guide, we will provide you with all the necessary information you need to know about rental income tax in Kenya. We will cover topics such as how rental income is taxed, deductions and allowances available for property owners, filing requirements, deadlines, and penalties for non-compliance. By the end of this guide, you will have a clear understanding of your obligations as a property owner in Kenya when it comes to rental income tax.

1. Introduction: What is Rental Income Tax and Who Needs to Pay It?

Rental income tax is a type of tax that is imposed on individuals or corporate entities who earn rental income from their properties. It is a tax levied on the amount of money earned from renting out property, including houses, apartments and commercial buildings.

The tax charged on rental income depends on whether you are an individual landlord or a corporate entity.

2. Corporate Rental Income Tax

For companies, rental income is taxed at the standard corporate income tax rate of 30%. Companies can claim deductions for rental property expenses to reduce their taxable income.

Landlords can claim certain expenses to reduce their taxable rental income. Allowable expenses include:

- Property management fees

- Property insurance premiums

- Repair and maintenance costs

- Utility bills related to the rental property

- Mortgage interest (for individual landlords only)

- Loan Interest

- Land Rates

To claim these expenses, landlords must keep proper records such as invoices and receipts. They will need to submit these documents to the Kenya Revenue Authority during tax filing.

Penalty, Interests and Late Submission of Corporate Rental Income Returns

Late filing of monthly rental income returns attracts a penalty of Ksh. 20,000 or 5% of the tax due whichever is higher for corporate entity.

Interest of 1% per month on the unpaid tax for late payment is incurred also.

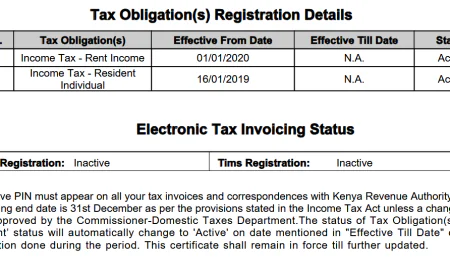

3. Resident Rental Income Tax

This type of tax is imposed to a resident whose income is accrued in or derived from Kenya for the use or occupation of residential property, and which is in excess of Ksh.280,000 thousand shillings but does not exceed Ksh. 15,000,000 million shillings during any year of income.

Resident Rental Income Rate in Kenya

The rate of tax in respect of residential rental income is 7.5% of the gross rental monthly income of a taxable resident person.

Submission of Rental Income Returns

A person subject to residential rental income should submit a return and pay the tax due on or before the 20th day of the month following the month which the rent is received.

A NIL return filling can be submitted in cases whereby a landlord does not receive any rent in that particular month.

Penalty, Interests and Late Submission of Returns

Late filing of monthly rental income returns attracts a penalty of Ksh. 2,000 or 5% of the tax due whichever is higher for resident individuals and Ksh.20,000 or 5% of the tax due whichever is higher for corporate entity.

Interest of 1% per month on the unpaid tax for late payment is incurred also.

4. Conclusion

In summary, rental income in Kenya is subject to personal income tax for individuals and corporate income tax for companies. However, allowable property-related expenses can reduce the taxable amount of rental income. Proper record keeping of expenses is important for landlords to minimize their rental income tax liability.

Was this information helpful ?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0